NACS Vice President of Research & Education Lori Buss Stillman stressed during her presentation at the NACS State of the Industry Summit in Dallas that all the information and insights at the event serve a bottom-line purpose: “We’re here to learn from the past to plan for the future.”

“This is not about rehashing what has already happened—it’s about recognizing the conditions that impacted our businesses and learning how to take advantages of the opportunities those conditions created,” said Stillman, noting that the basic building block of our industry is the transaction.

“Whether it’s inside your stores or at the forecourt, everything you do should be about growing transaction counts and growing basket value,” she said, adding, “Leave no stone unturned when looking for incremental transactions.”

Inflation’s Broad Impact

Inflation peaked in June 2022 at 9.1% according to the Consumer Price Index (CPI) and ended the year at an average of 8%. Inflation sits at 5.0% for the 12 months ending in March 2023, which is good news, but don’t look for the 2% interest rates from the last decade to return anytime soon.

“Although inflation has been moderating in recent months, the process of getting inflation back down to 2% has a long way to go and is likely to be bumpy,” Jerome Powell, chairman of the Federal Reserve, told the Senate Banking Committee in March.

Consumers have shown resilience, but for how much longer? Credit card debt hit a record $930 billion in 2022. Consumers are concerned about their financial health, with 60% saying they are cutting back or plan to cut back on discretionary spending due to rising financial pressures, according to AlixPartners. Those reduced purchases will come from retail, restaurants, travel, grocery spending and leisure activities.

The rise in interest rates has created new headwinds for businesses. A Bloomberg survey found that 48% of executives said that their company has been severely or very impacted by interest rates and the inflationary environment.

No doubt this one-ton elephant is still sitting in the room—or your store—and putting spending pressure on your business and your customers.

But convenience retailers have demonstrated throughout history that ours is a resilient industry. At the NACS State of the Industry Summit, more than 650 stakeholders heard how industry sales—even when adjusted for inflation—proved that tough economic times are opportunities to deliver what customers want, when they want it and where they are.

Inflation’s Impact on Convenience Retail

When inflation was beginning to increase in 2021, NACS created a model to calculate a Convenience Consumer Price Index that contains the categories that make up more than 85% of merchandise sales. The curve began to accelerate in August 2021 and grew steeper, reaching a 9.1% inflation rate by December 2022.

When inflation was beginning to increase in 2021, NACS created a model to calculate a Convenience Consumer Price Index that contains the categories that make up more than 85% of merchandise sales. The curve began to accelerate in August 2021 and grew steeper, reaching a 9.1% inflation rate by December 2022.

Unadjusted merchandise sales saw outstanding sales growth from January 2021 through the end of 2022—some months saw merchandise sales improve more than 10% year over year. However, when adjusted for inflation, merchandise sales tell another story.

Merchandise sales had a negative performance in 11 months over the past two years after pricing adjustments. This gap grew considerably wider during Q4 of 2022, capping off the year with 9+ point gap in both Q3 and Q4.

In 2021, the convenience CPI model estimated that the average annual inflation was 3.3%, and this number increased to 7.9% in 2022. “This [7.9%] number is your benchmark for merchandise—if your company was over 7.9% growth in merchandise that’s solid growth that’s likely marginal unit or mix growth,” she said.

“The reality is that after adjusting for inflation, merchandise sales were flat to down for most months throughout 2022,” said Stillman.

Inflation also had a significant impact on foodservice.

The gaps between unadjusted and adjusted foodservice sales were larger than what the industry experienced with merchandise. Inflation also moved faster for foodservice and reached +10.3% in Q4 of 2022.

If your company’s foodservice sales growth was 9.7% or better, there was likely some unit or mix growth.

In 2021, the average annual foodservice convenience CPI saw an increase of 5.5%, and with a full year of inflation under the industry’s belt, the average foodservice CPI increase for 2022 was 9.7%. “If your company’s foodservice sales growth was 9.7% or better, there was likely some unit or mix growth,” said Stillman.

Other retail channels also grew sales quickly due to the inflationary environment. The exception was drug stores, which registered a modest 2.7% sales growth, well below inflation. The channel has closed 1,000 sites for a 2.5% decrease in total store count over two years.

Fuel Prices Up, Volumes Flat

The story of retail fueling in 2022 came down to pricing. “Essentially all sales increases in terms of dollars were price driven,” said Stillman, adding that volatility in crude oil sent gasoline prices soaring.

Estimated industry fuel sales increased 41.2% reaching $603.2 billion, largely as a result of higher gasoline prices, which increased 33.1% to an average of $4.06 in 2022—up from an average of $3.05 in 2021.

Transactions Hold Their Ground

The good news around transaction counts is that they’re on the right path. Total industry transactions had declined every year from 2016 until 2021, a year that experienced a COVID-19 rebound.

In 2022, inside transaction count growth resumed after a general trend of decline since 2016. “Thinking back to last year’s SOI Summit, the goal was to get back to 2019 levels on inside transactions,” said Stillman, adding that total transactions in 2022 were outpacing 2020 and 2021 during most months, which is great news for the industry.

“We should all go back and celebrate with our frontline employees. This is a big win for everyone in this room,” Stillman said.

Basket value, a combination of inside merchandise and foodservice, held steady in 2021 but started to show signs of inflationary pressure by the end of the year. In 2022, however, it was off to the races as prices increased and basket value followed, even as transaction counts increased.

Controlling Expenses

Inside store operating profit (excluding gross profits, expenses and card fees related to the fuel component of a site) declined, as direct store operating expenses (DSOE) grew at a faster rate than inside gross profit dollars.

In 2022, average inside operating profit declined by 50% to $111 per store, per month. This also means that the $7.52 average basket value experienced a 34-cent loss of inside store operating profit.

“This metric can be unforgiving,” said Stillman, adding that operating expenses are the main difference between 2021 and 2022. “If operating expenses had held flat, basket value in 2022 would have broken even.”

Higher Wages Don’t Improve Turnover

Finding a way to control labor costs is a top concern for convenience retailers, and 2022 proved to be another challenging year. Unemployment remained at historic lows (3.3% in December 2022) and thousands of jobs were unfilled.

Although non-manager turnover shrunk by a little less than a point, manager turnover trended the opposite way, increasing by 2.5 points to 34.9%. “They’re being actively recruited because other operators know that if you can be a good convenience store manager, there’s not a job that they’re not going to do well,” Stillman said. “Really pay attention to your managers.”

Compared to other retail channels, convenience retailers consistently outspend to attract and retain employees, with total compensation (wages and benefits) increasing at a much higher rate.

Amid this trend of outspending to attract and retain employees, NACS data shows that almost 8 of 10 separations were voluntary, which reflects culture in a company’s offices and its stores.

“Convenience retailers that have a reputation for being great places to work also have an edge when it comes to workplace culture. These companies are able to keep their turnover rates well below 100%, even in this environment,” said Stillman.

Top Performers Enjoy the Apex

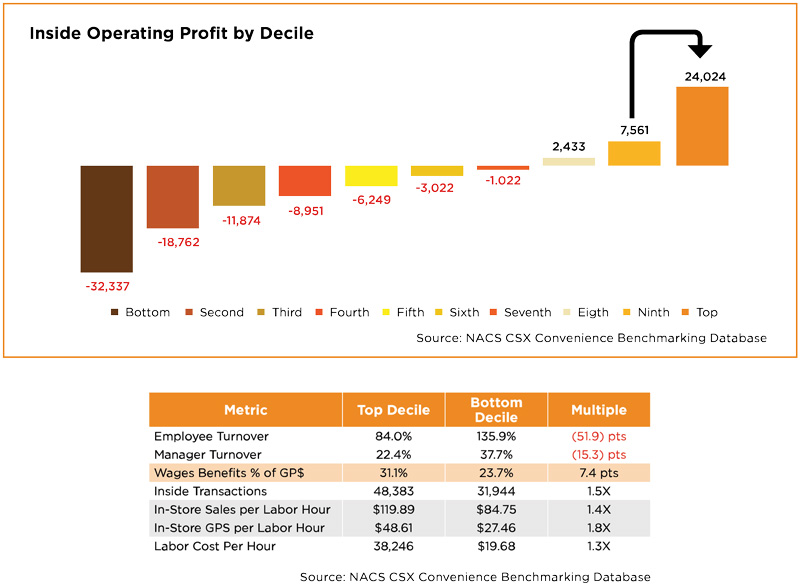

Looking at data from top industry performers is a great way for other retailers to see how the best in the business are faring. NACS generates this by ranking all the companies that submit SOI survey data by their calculated store operating profit (minus cost of goods, facility expenses and DSOE; including fuel gross profit dollars and expenses from selling fuel).

When fuel gross profits are stripped from the store operating profit equation, only the best operators profit.

“If you really want to compare to the best of the best, this is it. Not only is there a $56,000 monthly swing of inside store operating profit between the top and bottom deciles, the top decile has a 3.2 times multiple for inside store operating profit versus the next best decile,” said Stillman.

The rubber really hits the road for top performers on store profitability when it comes to foodservice. These companies sold 5.5 times the bottom on foodservice and conducted 1.4 times the total transactions. Top performers also generated 6.9 times foodservice gross profit dollars versus the bottom.

“Of course, more complex operations have more services, and more food prep will result in higher wages,” said Stillman.

The top performers enjoyed much lower turnover, but wages and benefits were a considerably larger drain on gross profit dollars—these retailers pay almost $6 per hour more in total compensation than companies at the bottom, which are about 30% higher.