“Amazing. Unprecedented. Historic.” Those are the words Chris Long used to describe the performance of alcoholic beverages in convenience stores in 2020. Long, director of category management–age verified at Kum & Go, which has 400 stores in 11 states primarily in its home state of Iowa, discussed the double-digit growth that the beer, wine and liquor categories all enjoyed in c-stores, largely attributed to shifts in consumer buying patterns brought on by the pandemic, as well as fast-growing new products that are ideal for the channel.

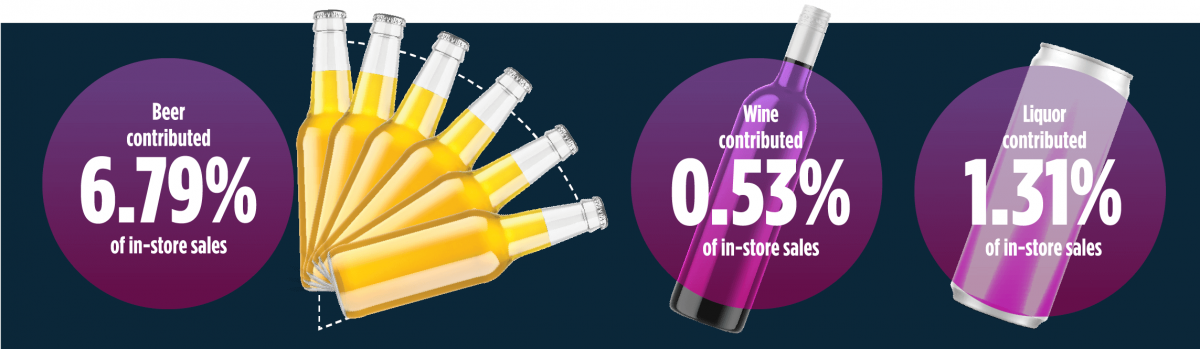

According to NACS State of the Industry data, alcoholic beverages comprise 8.6% of total inside c-store sales and contribute nearly 4.9% to margin. The importance of beer, wine and distilled spirits to basket rings and profitability was certainly highlighted last year, at a time when other in-store departments were hampered. The tailwinds that the pandemic wrought on bars and restaurants translated into opportunity for convenience retailers, Long said. “Consumers came to rely on c-stores for stock-up trips, especially for alcohol.”

Among the shifts in consumer habits that benefitted alcoholic beverages in 2020 were large pack-size purchases, increased at-home mixology and more outdoor activities that called for convenient packaging, such as canned wine. Moreover, emerging ready-to-drink products such as hard seltzers and canned cocktails continued to surge, in part driven by increased demand for low-carbohydrate, low-sugar, low-calorie drinks. “They allow consumers to have a taste of mixology in their own homes,” Long said.

FMBs, Large Packs Soar

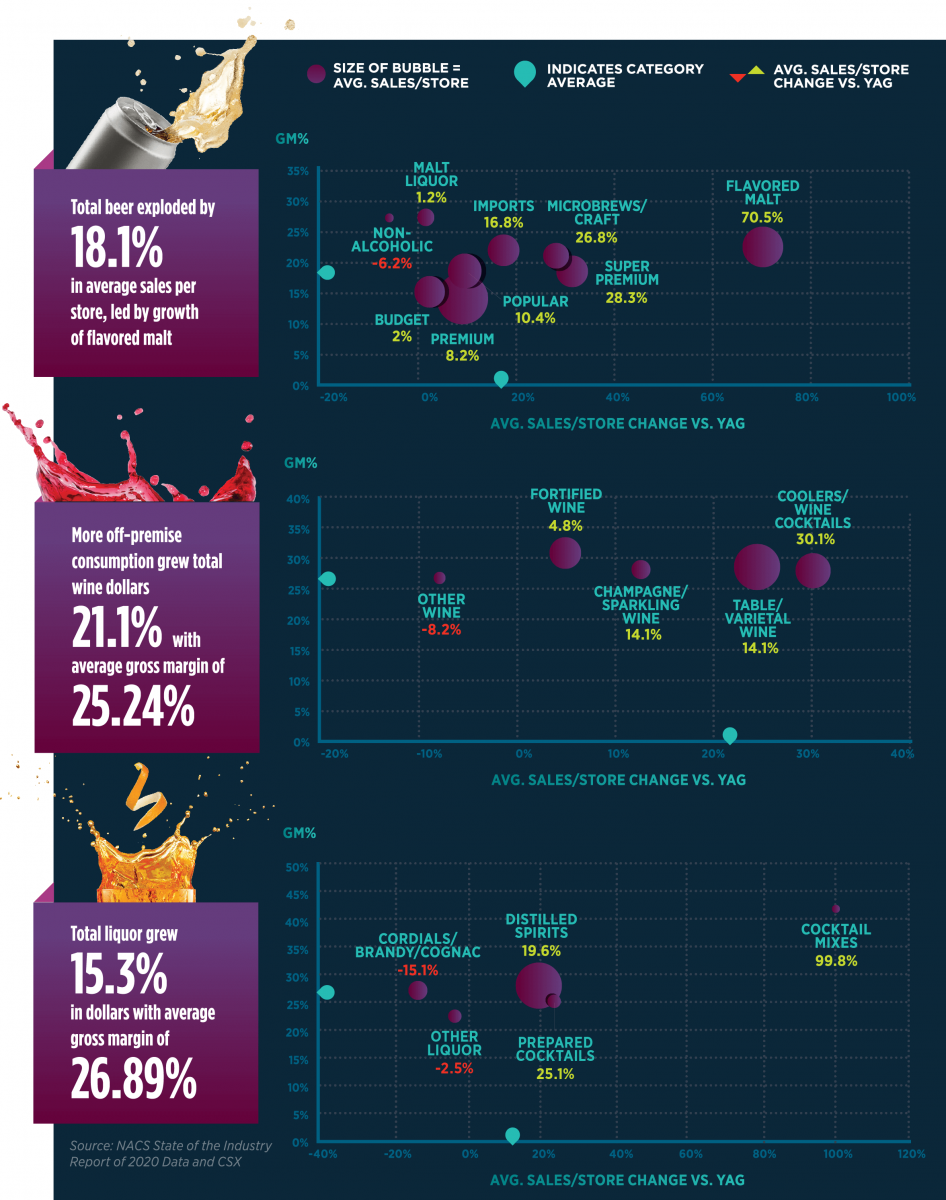

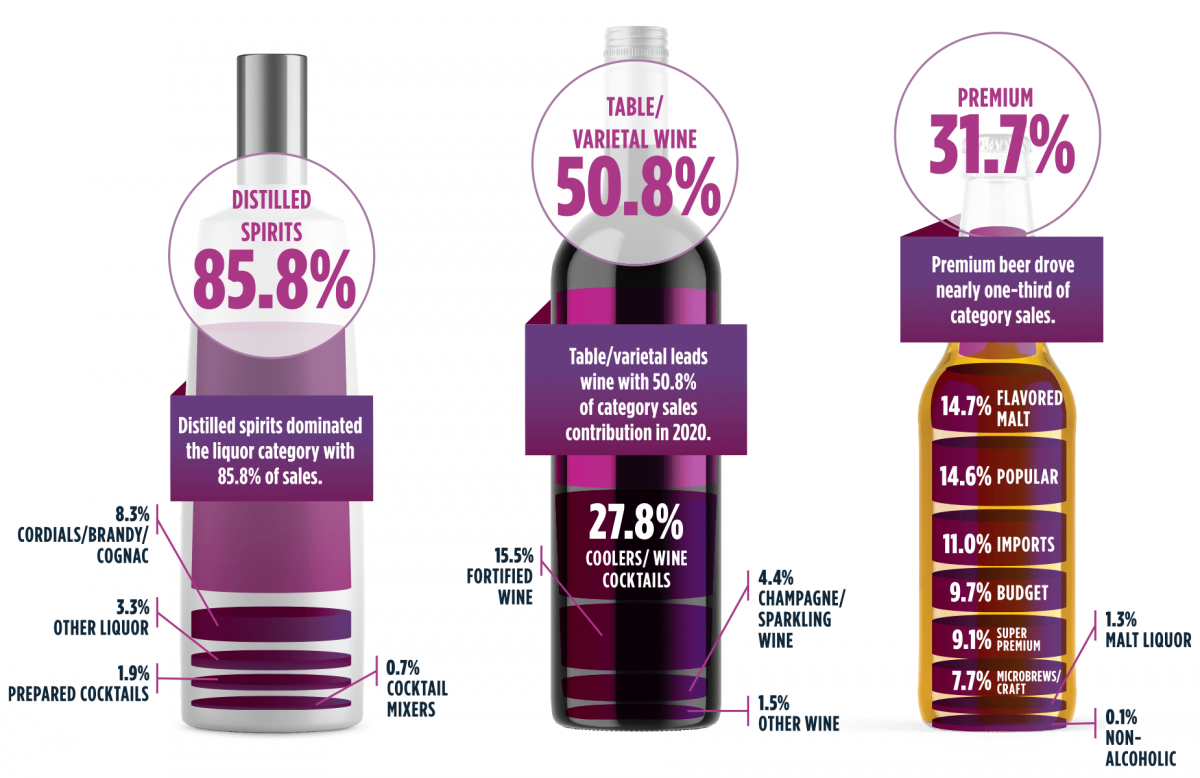

Average store sales of beer jumped 18.1% last year, growth which Long called unprecedented. “Our fast trip worked for us in helping to fill consumer needs,” he said. Flavored malt beverages (FMBs) emerged as the subcategory superstar, with average store sales surging 70.5%. That pushed FMBs into the No. 2 position among beer subcategories with 14.7% of category sales, behind only premium beer, which increased 8.2% and accounts for nearly one-third of category sales.

Dramatic consumer shifts from six-pack purchases to 12-, 24- and 30-packs propelled basket rings higher. Variety packs, particularly for hard seltzers, flew off shelves. “Variety packs allow c-stores to better utilize space, as one 12-pack variety pack can replace two to three SKUs,” Long remarked. “Singles were relatively flat,” he said.

Hard seltzers and other FMBs are having their moment in c-stores and other retail channels. “Hard seltzers turned in an incredible performance in 2020,” Long said, and “drove FMBs to amazing heights.” The subcategory’s 70.5% growth aside, FMBs are driving beer’s profitability mix. According to the SOI, FMBs contribute a 22.87% gross margin, as compared to an overall category average of 18.44%. “That’s what makes this new innovative category so appealing to us,” he noted of the above-premium-priced brands.

Big Opportunity Gap

Among alcoholic beverage categories, wine posted the best performance in c-stores last year as average store sales surged 21.1%, delivering average gross margins of 25.24%. Still, wine only accounts for 0.53% of in-store sales and just 0.37% of in-store gross-margin contribution. “We have a large opportunity,” Long said, noting that wine sales in the c-store channel have plenty of room to grow.

Table/varietal wine—which jumped 24.2% in average sales per store thanks to the loss of some on-premise occasions at bars and restaurants—accounts for more than half of total wine sales in c-stores, followed by coolers and wine cocktails at 27.8%. The coolers/wine cocktails subcategory, meanwhile, was the fastest growing within the category last year as average sales increased 30.1% in 2020 off a relatively large base in 2019.

Nontraditional wine packages, including cans, large-format boxes and tetra packs, are trending, driven by consumer demand for more convenient options than bottles. The shift offers c-store retailers a big opportunity. “Small bottles and large-format boxes fit right in our wheelhouse, due to space restrictions,” Long said.

High Spirits

Average store sales of liquor increased 15.3% last year, according to SOI data, fueled in part by a 19.6% gain for distilled products and a 25% increase for prepared cocktails. Liquor accounts for only 1.31% of total in-store sales—due to legal restrictions in many states—and 1.15% of in-store gross margin contributions. At stores that sell liquor, average gross margins run 26.89%, Long said. Among the trends convenience retailers are seeing within the category is a shift from budget and value tiers to more premium-priced spirits such as whisky and Tequila.

The stay-at-home economy helped propel sales of prepared cocktails. “RTD cocktails offer opportunity for suppliers and retailers alike,” he remarked. Relatedly, average store sales of cocktail mixes doubled last year, as “shoppers looked to fill the gap that on-premise restrictions created with cocktails at home,” Long said.

With products like RTD cocktails, adult milkshakes and smoothies, innovation within the category is only expected to continue, further blurring the lines between liquor and beer.

Key Fundamentals

To ensure that the strong trends for beer, wine and liquor in c-stores continue in 2021, Long advised retailers to merchandise for local events and seasonal occasions and provide proper product organization and shelf flow. Lean into limited-time-only offerings to “drive excitement,” as well as larger pack sizes. Cross-category tie-ins and twofer offers, meanwhile, help build larger baskets, Long said, and clearly communicated pricing is imperative. When it comes to space, he recommended retailers consider secondary locations to drive impulse purchases and to utilize vendor point-of-sale “to add pop.”

While the past year has been one of dramatic change for the beer, wine and liquor categories, retailers must still adhere to the basics, Long said. “The fundamentals are still key—price, product, promotion and platform.”