Riddled with regulatory challenges—notably vape product flavor bans—cigarettes and other tobacco products face more burn on Capitol Hill and in statehouses than any other product convenience stores sell.

Customers turned to cigars as a product to kick back and relax with.

The biggest disruption came in late December 2019, when President Donald Trump signed into law legislation that makes it illegal for retailers to sell tobacco products to anyone younger than 21. More than a decade of declining smoking rates and increasing excise taxes on cigarettes have been two constant hurdles for cigarettes. In 2019, industry sales of cigarettes dipped 1.9% year over year as the percentage of in-store sales also lost 1.3 share points from 2018. In 2020, the law could have been a third hurdle to dent consumption and sales.

But that was not the case.

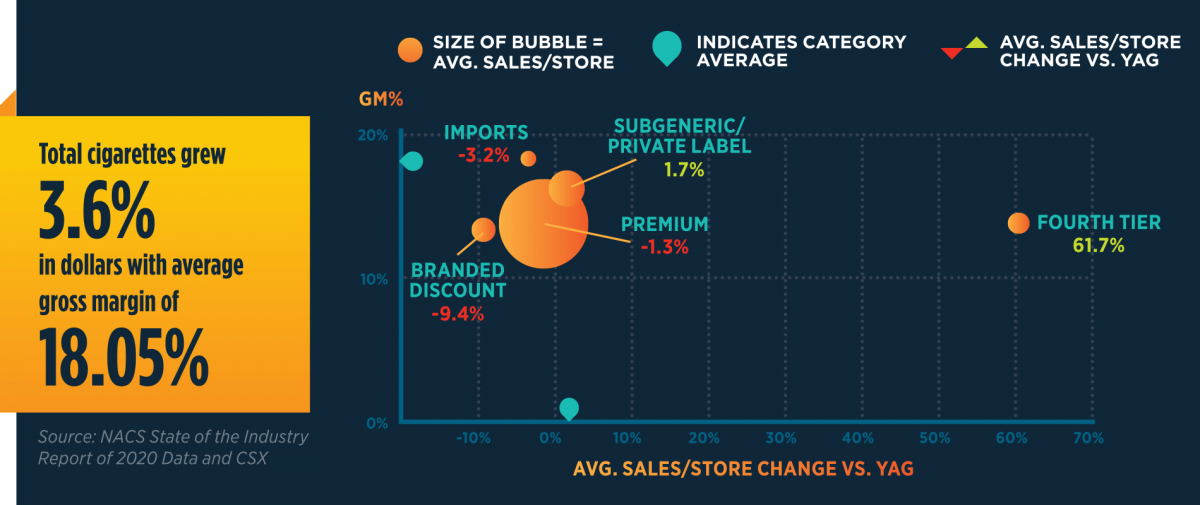

Cigarettes are a declining category but continue to be a top sales and profit generator for convenience stores, increasing 3.6% in sales year over year in 2020. The other tobacco products (OTP) category, meanwhile, grew 4.5% in 2020, but one subcategory—e-cigarettes—took a nosedive for the first time since hitting the U.S. market.

Cigarette Sales Rise

The pandemic year generated a notable split between premium- and lower-tier subcategories, shared Laura White, category manager for cigarettes at Atlanta, Georgia-based RaceTrac.

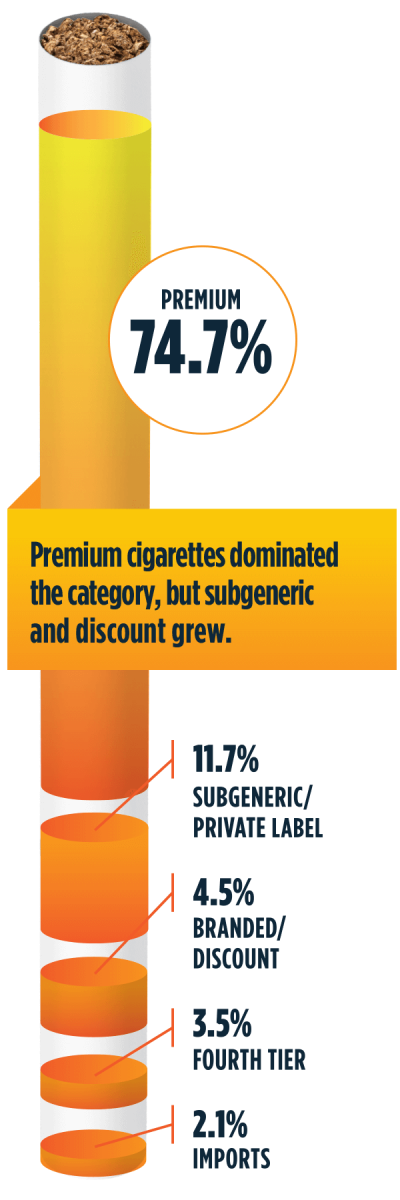

Premium cigarettes—the lion’s share of the category at 77.5% of the category’s total sales—decreased sales 1.3% but increased gross profit. Fourth-tier cigarettes increased in double digits for both sales (61.7%) and gross profit (89.9%), although they only represented 3.5% of total category sales.

This bifurcation among top-tier and bottom-tier brands was driven by changes in consumer behavior, as more people were working from home, dining at home, driving less and adapting their social routines to pandemic realities.

Last year, cigarettes experienced one of the biggest twists during a chaotic year full of atypical highlights. NACS CSX data showed that in 2020, cigarette sales were up about 4.4% from January through August. By comparison, cigarette sales were down 0.6% from January to August 2019.

To continue the trajectory, White discussed four industry priorities to maintain the momentum cigarette sales gained during 2020.

Opportunities

“Retailers should be using the momentum in sales that we have now to continue growth for 2021,” said White, suggesting that retailers look no further than their point-of-sale (POS) data to make informed decisions and keep up with current trends and sales patterns.

Subgeneric/private-label cigarettes, which experienced growth the past four years, was the second largest category contributor in 2020 and represented 11.7% of category sales. Branded discount, fourth tier and imports rounded out the category.

Consumers and retailers typically plan for two cost increases per year. However, 2020 saw four cost increases. “These cost increases will push consumers to the lower-price-point brands and increase the fourth-tier private-label brands,” said White, suggesting that retailers evaluate how they can continue reaching customers who are minding their spend and finances by promoting brands that fit their desired price point.

There are also opportunities to upsell, particularly to larger pack sizes. “Consumer purchasing changed during the coronavirus pandemic,” said White, suggesting that multipacks will allow shoppers to continue stocking up until a sense of normalcy returns.

Promotions

Successful promotions rely on staff communication. “If your staff doesn’t understand the program, they’re not going to be able to sell it,” said White, adding that awareness is equally important so staff can adequately communicate the promotion to customers.

“And once you’ve run a promotion, make sure you have a clear and concise way to measure its success and act on the learnings,” she said.

Assortment

Relying on POS data can help retailers expand beyond their core cigarette brands and products. Also, now may be a time to explore other partnerships with small or new distributors to better track innovations and trends within the category.

Allocation

Inside the store, 2020 was also the year where cleanliness became a top priority for consumers in deciding where to shop. “Make sure fixtures are clean, well-lit and the signage is clear,” suggested White.

At RaceTrac, she shared the company ensures correct counts, accounts for seasonality and plans around events to maintain inventory and space allocation. “It’s always great to rely on your employees to help track special events that may be a great opportunity to take advantage of near your stores,” she said.

OTP Benefits From Innovation

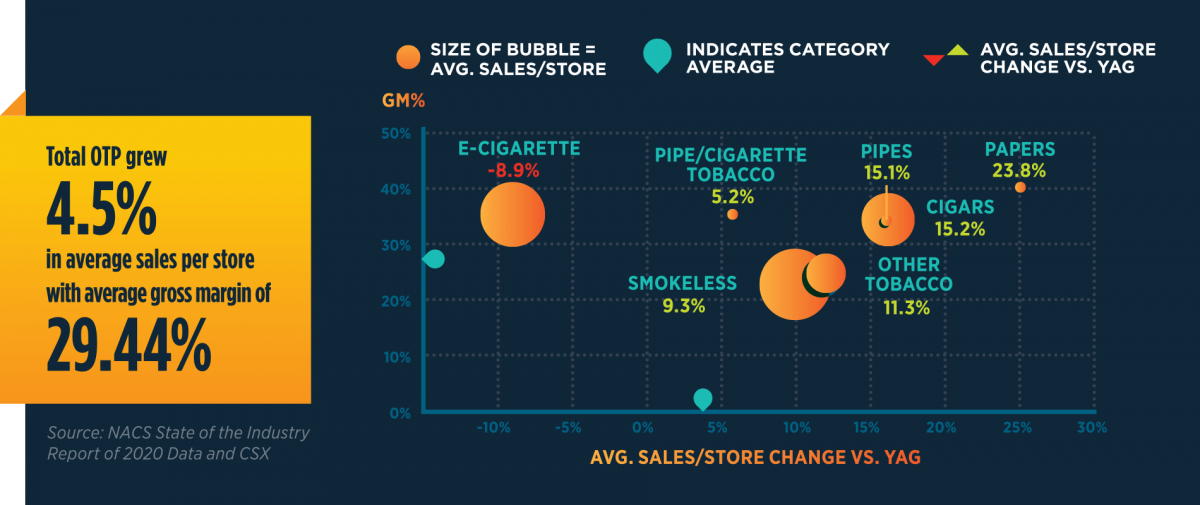

The OTP category grew 4.5% in 2020, led by increases in smokeless tobacco, cigars and other nicotine products. The category represented 6.9% of in-store sales and grew share 0.23 points from the prior year.

The category has benefited from innovation, with newer items such as nicotine pouches and alternative smokeless products piquing the interest of customers looking for alternatives to tobacco. Products like heat-not-burn tobacco have the potential to generate category excitement.

One shining star of the OTP category lost its luster: e-cigarettes. These products saw tremendous growth when they were introduced to the convenience channel and became an emerging product for retailers, attracting customers who were seeking an alternative to traditional tobacco products.

E-cigarettes faced a tumultuous regulatory environment in 2019. The U.S. Food and Drug Administration banned the sale of flavored, pod-based e-cigarettes—excluding tobacco and menthol flavors—across all retail channels.

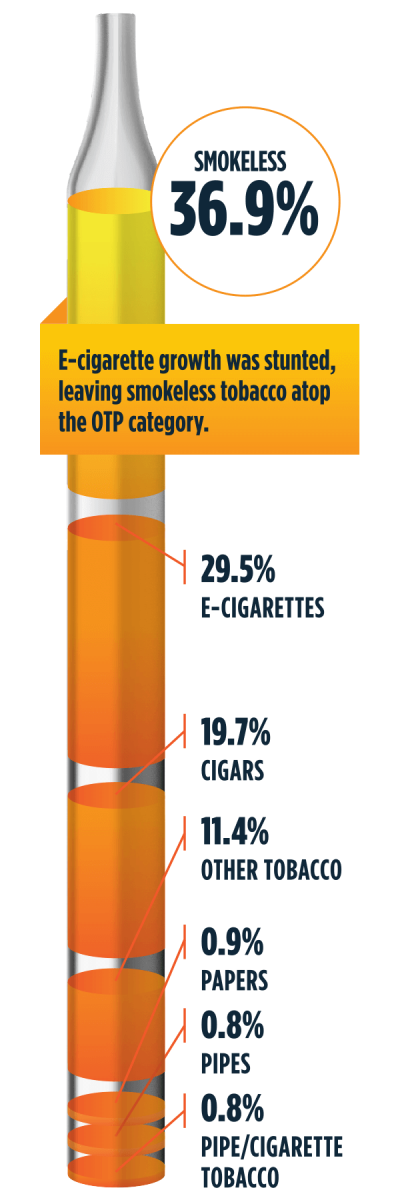

With flavor bans and health concerns, 2020 “wasn’t kind to vapor products,” said White. The subcategory lost share in terms of percent of total category sales, dropping from 33.9% in 2019 to 29.5% in 2020.

Smokeless tobacco products, OTP’s largest sales contributor, gained category share (35.2% in 2019 to 36.9% in 2020). Cigars also gained category share, increasing from 17.9% in 2019 to 19.7% in 2020. “It was a great year for products of indulgence, and customers turned to cigars as a product to kick back and relax with,” said White.

Moving forward, White shared areas to watch within the OTP category:

- Innovation: With overall trips down, new products such as heat-not-burn technology have not had the customer exposure of a typical year. “We don’t yet know how customers will react to and engage with this new product, or how quickly adoption will happen,” said White.

- Alternative tobacco: Products like pouches are providing customers even more options for nicotine consumption.

- Consumption changes: More people working from home means they can consume their tobacco product of choice anytime throughout the workday. “Retailers have to now figure out how to keep up with these changes in behavior to keep these loyal buyers,” she said, adding that these products will also fill a need for consumers as they head back to the workplace.

Convenience retailers can expect that 2021 will be the year for OTP category innovation, although the potential for regulatory setbacks is worth keeping an eye on.